Episode 21: Chip War

NVIDIA’s CEO Jason Huang, commenced GTC 2023 (GPU Technology Conference) by saying,

“For nearly four decades, Moore’s Law has been the governing dynamics of the computer industry, which in turn, has impacted every industry. Although “the exponential performance increase at constant cost and power has slowed down […], computing advance has gone to light speed.” The underlying factor is Artificial Intelligence (AI), and we should all pay attention.”

Given the prodigal invention of Chat-GPT which has confounded the world as a reckoning force of technological development, it makes sense to kickoff a global conference by mentioning Artificial Intelligence. But why does the leader of the world’s most advanced computing multi-national organization still pay homage to the Moore’s Law?

A quick internet search on Moore’s Law led me to the following: In 1965, Gordon E. Moore, the co-founder of Intel, made this observation that the number of transistors on a microchip doubles about every two years, though the cost of computers is halved. Today, thanks to Moore’s Law, semiconductors are embedded in every device that requires computing power. Most of the world’s GDP is produced with devices that rely on semiconductors. For a product that didn’t exist 70 years ago, this is an extraordinary ascent!

The undeniable stack of evidence on how computing power of chips has grown exponentially is seen through the lens of digitisation of entire nations today. Interestingly, as we enter an era defined by AI, Big Data and Internet of Things every firm will start manufacturing its intelligence and a country’s control on computing power will eventually become the cornerstone of international dominance.

Therefore, it is imperative to understand the risks that stem not only from the fragility of trade in the industry but from the audacious and potentially thinkable moves that can tip the scale towards a new world order.

Recent events have shown how globalisation can go wrong. While we continue to salvage and pacify the ill effects of the Russia-Ukraine war and the pandemic-induced monetary policy changes, a global plan of action, hidden in plain sight has begun and it seems to be focused on reworking of semiconductor supply chains.

Using FactSet’s Smart Search which runs a comprehensive search query on all content sets and unstructured data for the keyword “Semiconductors”

there is a considerable spike in results at the point of writing of this article,

(Source: FactSet)

With major news headlines about national support for the industry, there is significant positioning by major countries to maneuver the future of their country’s participation in the far-flung and bewilderingly complex supply chains. It is surely a repeat of a strategy that has historically yielded certain capabilities that are unseen in other industries, where governments elbow their way by subsidizing firms and funding training programs.

Headlines from the past few months signal how countries are focused on implementing programs to facilitate trade in various regions of the world-

“India’s prospects in the Global Semiconductor Manufacturing Race: iPhone supplier Foxconn will build a factory in India.”

“Semiconductor manufacturers seek a slice of $40 billion in new federal subsidies in America.”

“Japan to subsidize domestic chipmaking beyond the cutting edge/”

“Samsung Electronics announced that it plans to invest 300 trillion Korean won ($228 Billion) in a new semiconductor complex in South Korea.”

The company that fabricates the processors for the world’s most valuable entity, whose products are etched with the following text- “Designed by Apple in California. Assembled in China.” is TSMC (Taiwan Semiconductor Manufacturing Company), located on a tiny island in the strait of Taiwan that sits on the Chelungpu fault.

(Source: FactSet)

For some context, chips from Taiwan provide 37 percent of the world’s new computing power each year. Two Korean companies produce 44 percent of the world’s memory chips. The Dutch company ASML builds 100 percent of the world’s extreme ultraviolet lithography machines, without which cutting-edge chips are simply impossible to make. Definitely, OPEC’s 40 percent share of world oil production looks faint by comparison.

The United States has held a stranglehold on the silicon chips that gave Silicon Valley its name. Today, nearly every major data center uses x86 chips from either Intel or AMD, a near monopoly over data center chips. (The cloud can’t function without their processors) But as China’s geopolitical clout grows, the U.S. fears that they’d shortly form the backbone of the chip industry. Strategists in Beijing and Washington now realize that all advanced tech—from machine learning to missile systems, from automated vehicles to armed drones—requires cutting-edge chips.

China’s increasing presence and dominance over Taiwan poses a threat. Encouraged potentially by Russia’s audacious efforts over Ukraine. It seems like China’s ruling party can aim to assert control over Taiwan. The Anti-Secession Law, (unilaterally enacted by China—claims that Taiwan is a part of China and suggests that non-peaceful means may be arbitrarily employed by China to achieve unification) potentially can be a “non-peaceful means” in the Taiwan Strait and can be the cause of clash of great powers.

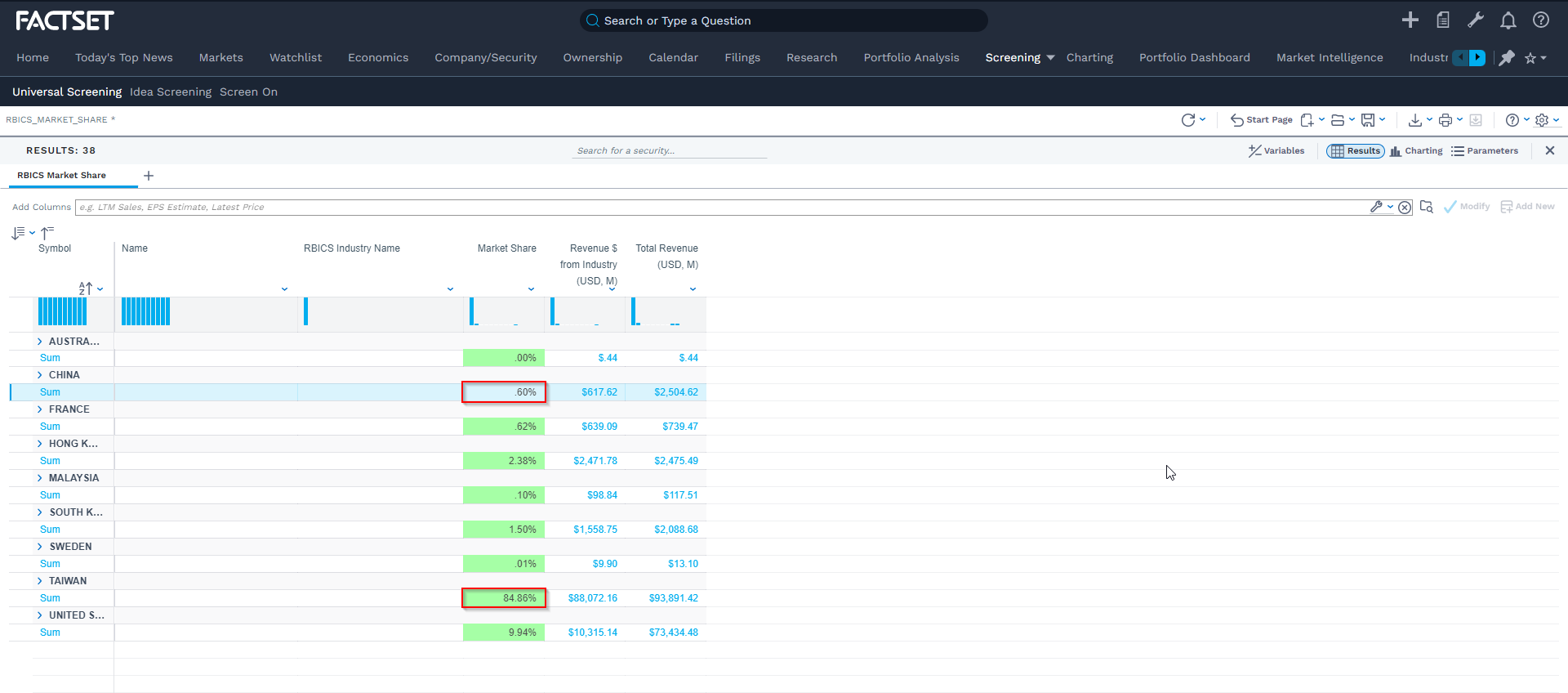

Below, FactSet’s Revere Geographic Revenue Exposure (GeoRev) database, provides visibility into individual exposure to World/Semiconductors Industry by regions across the world.

With just 0.60% of the world’s Market Share of semiconductor foundry business, China’s efforts to capitalize on the 85% of the pie are ambitious at best, and a major threat to the U.S. supremacy.

(Source: FactSet)

As Chris Miller puts up a cogent argument through his book Chip War: The Fight for the World’s Most Critical Technology,

“World War II was decided by steel and aluminum, and followed shortly thereafter by the Cold War, which was defined by atomic weapons. The rivalry between the world powers may well be determined by computing power. Both Washington and Beijing are fixated on controlling the future of computing - and to, a frightening degree, that future is dependent on a small island that Beijing considers a renegade province and America has committed to defend by force.”

(Source: FactSet)

Most smartphone processors are fabricated in Taiwan as are many of the chips that go into a typical phone or pc. Today, no company besides TSMC has the skill or the production capacity to build the chips Apple needs. The world economy and the supply chains that crisscross the globe are predicated on the precarious peace of the Taiwan Strait.

The risks that imperil the essential choke points of the semiconductor industry and globe’s supply of chips can take the following forms:

TSMC’s fabs slip into the Chelungpu Fault. (The last big Earthquake was in 1999); the reverberations would shake the global economy. The world’s computing power falls to 63% of capacity the following year.

If a war knocks out TSMC’s fabs. A Chinese air and missile campaign could alone defeat Taiwan’s military and shut down the country’s economy without placing a single pair of Chinese boots on the ground. Many industries will face debilitating chip shortages.

Seemingly every company on either side of the Taiwanese Strait, from Apple to Huawei bets on precarious peace. Until these risks materialize, “Peace in the Taiwan Strait is to every country’s benefit.”

Overall, it will be interesting to see how the future pans out for the industry, within the sphere of ubiquitous computing, rollout of the next generation of infrastructure and machinery to produce remarkable chip designs and solutions. If data in the 21st century is the new currency, the semiconductor and chip industry is the spectrum of networks and infrastructure that facilitates the flow of movement, usage and storage.

Chris Miller’s book, Chip War is a great book on tech that isn’t about software!